Now Reading: Common Myths About Islamic Personal Loans Debunked

-

01

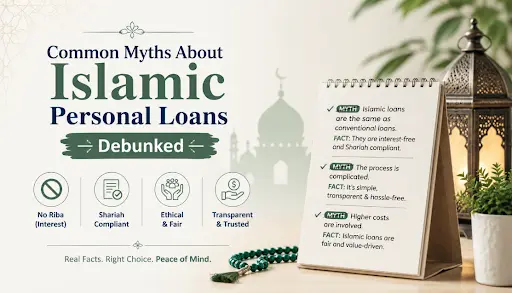

Common Myths About Islamic Personal Loans Debunked

Understanding the Truth About Islamic Personal Financing in the UAE

As demand for ethical and Shariah-compliant financial solutions continues to grow, more residents are exploring options for an Islamic loan in UAE. However, despite their increasing popularity, Islamic personal financing products are often misunderstood. Many people assume these financing solutions are only available to Muslims, come with hidden costs, or function exactly like conventional loans under a different name.

These misconceptions can prevent individuals from making informed financial decisions. Understanding how Islamic personal financing works can help borrowers choose solutions that align with both their financial goals and ethical values.

In this article, we debunk some of the most common myths surrounding Islamic personal financing and explain the facts behind Shariah-compliant lending practices.

Visit For More Updates: Trippin UAE

What Is an Islamic Personal Loan?

Before addressing the myths, it is important to understand what Islamic personal financing is.

Unlike conventional lending, Islamic financing follows Shariah principles, which prohibit the charging or payment of interest (Riba). Instead, financial institutions structure financing through approved Islamic contracts that focus on transparency, asset-backed transactions, and mutually agreed profit arrangements.

These financing solutions are designed to promote fairness, ethical conduct, and responsible financial management while meeting personal funding needs such as education, travel, home improvements, debt consolidation, or other expenses.

Myth 1: Islamic Personal Loans Are Only for Muslims

Fact: Anyone Can Apply for Islamic Financing

One of the most widespread misconceptions is that Islamic financing products are exclusively for Muslim customers.

Islamic financial products are available to individuals of all faiths and backgrounds. Many non-Muslim residents choose an Islamic loan in UAE because they appreciate its transparent structure, ethical principles, and clearly defined terms.

Islamic financing focuses on responsible lending practices and transparency, making it an attractive option for anyone seeking an alternative to conventional borrowing.

Key Takeaway

Islamic personal financing is open to eligible applicants regardless of religion or nationality.

Myth 2: Islamic Loans Are the Same as Conventional Loans

Fact: The Financing Structure Is Different

Although both Islamic and conventional financing provide access to funds, their underlying structures differ significantly.

Conventional loans are generally based on interest charges that accumulate over time. Islamic financing, on the other hand, operates through Shariah-compliant contracts where the profit rate, payment obligations, and financing terms are clearly agreed upon from the beginning.

This approach emphasizes transparency and reduces uncertainty for both the customer and the financial institution.

Key Takeaway

Islamic financing is based on ethical financial principles and approved contractual structures rather than interest-based lending.

Myth 3: Islamic Financing Is More Expensive

Fact: Costs Depend on the Product and Terms

Many borrowers assume that Islamic financing automatically costs more than conventional borrowing.

The reality is that financing costs vary based on factors such as:

- Financing amount

- Repayment period

- Applicant profile

- Profit rate structure

- Market conditions

In many cases, the overall cost of Islamic financing can be competitive with traditional lending products.

Rather than focusing solely on assumptions, borrowers should compare financing options carefully and review all terms before deciding.

Key Takeaway

Islamic financing is not inherently more expensive. The total cost depends on the specific financing arrangement.

Myth 4: Islamic Personal Loans Involve Hidden Charges

Fact: Transparency Is a Core Principle

Transparency is one of the fundamental principles of Islamic finance.

Shariah-compliant financing contracts generally require clear disclosure of:

- Financing amount

- Profit rates

- Repayment schedule

- Applicable fees

- Contract terms

This emphasis on clarity helps customers understand their obligations before entering into an agreement.

As with any financial product, borrowers should always review documentation carefully and ask questions about any charges or conditions they do not understand.

Key Takeaway

Islamic financing promotes transparency and clear communication of financial obligations.

Myth 5: Approval Takes Much Longer Than Conventional Loans

Fact: Digital Processes Have Improved Efficiency

Years ago, some borrowers believed Islamic financing involved lengthy paperwork and slower approval times.

Today, many financial institutions use digital application systems, online verification tools, and streamlined approval processes.

As a result, obtaining a Sharjah Islamic bank personal loan alternative or any other Islamic financing solution may be just as efficient as applying for conventional financing, provided the applicant meets eligibility requirements and submits complete documentation.

Key Takeaway

Modern Islamic financing applications are often processed quickly through digital channels.

Myth 6: Islamic Financing Offers Limited Flexibility

Fact: Various Financing Options Are Available

Another misconception is that Islamic financing products are highly restrictive.

In reality, Islamic personal financing can support a wide range of legitimate personal needs, including:

- Education expenses

- Medical costs

- Travel requirements

- Home renovation projects

- Family-related expenses

- Debt management needs

Different financing structures are designed to accommodate diverse customer requirements while remaining compliant with Shariah principles.

Key Takeaway

Islamic financing offers flexibility for various personal financial goals.

Myth 7: Islamic Financing Is Outdated

Fact: Islamic Finance Is a Modern Global Industry

Islamic finance has evolved into a sophisticated global financial sector serving millions of customers worldwide.

Financial institutions continually invest in:

- Digital banking services

- Mobile applications

- Online financing platforms

- Automated customer support

- Enhanced security systems

The combination of traditional ethical principles and modern financial technology has helped Islamic finance become a preferred choice for many consumers.

Key Takeaway

Islamic financing combines established ethical principles with modern banking innovation.

Myth 8: Profit Rates Are Unpredictable

Fact: Terms Are Usually Agreed Upon Upfront

Some borrowers mistakenly believe Islamic financing involves uncertainty regarding repayment obligations.

In practice, financing contracts generally specify:

- Repayment schedules

- Profit calculations

- Monthly installment amounts

- Financing duration

Knowing these details upfront allows customers to plan their budgets more effectively.

Key Takeaway

Islamic financing emphasizes clarity and predictability in repayment arrangements.

Why More UAE Residents Are Choosing Islamic Personal Financing

Interest in Islamic financing continues to grow because many consumers value:

- Ethical financial practices

- Transparent contracts

- Responsible lending principles

- Clear repayment structures

- Shariah-compliant financing solutions

As awareness increases, more residents are exploring options for an Islamic loan in UAE to meet personal financial requirements while maintaining alignment with their values.

The growth of digital banking and customer-focused services has also made Islamic financing more accessible than ever before.

Frequently Asked Questions

Can non-Muslims apply for Islamic personal financing?

Yes. Islamic financing products are available to eligible applicants regardless of religion.

Is Islamic financing interest-free?

Islamic financing does not charge interest in the conventional sense. Instead, approved Shariah-compliant structures use agreed profit arrangements and transparent contractual terms.

Is Islamic financing available online?

Many financial institutions now offer online applications, digital document submission, and remote approval processes.

How do I choose the right Islamic financing option?

Compare financing terms, repayment schedules, eligibility requirements, fees, and overall affordability before deciding.

Understanding Islamic Finance Beyond the Myths

Misconceptions about Islamic personal financing often create unnecessary confusion for borrowers. The truth is that modern Islamic financing solutions are transparent, accessible, and designed to meet diverse personal financial needs.

Whether you are researching an Islamic loan in UAE or comparing options like a Sharjah Islamic bank personal loan, understanding the facts can help you make a more informed decision.

By focusing on transparency, ethical financial practices, and clearly defined terms, Islamic personal financing continues to provide a trusted alternative for individuals seeking responsible and Shariah-compliant funding solutions.